America at 250: Is Your Retirement Strategy Anchored in the Past or Built for the Future of Longevity?

This June 2026, America is turning 250.

It is a monumental milestone. A moment to celebrate a quarter-millennium of innovation, courage, and growth. Yet, it is also a powerful diagnostic reminder of how fundamentally life itself has changed. When this nation was founded in 1776, most families were not preoccupied with tax-efficient withdrawal strategies, Roth conversions, or whether they had sufficient liquidity for a 30-year active retirement. Their focus was immediate and primal: clean water, surviving infection, childbirth risks, food security, and fundamental survival. Retirement, as we define it today—a distinct phase of life dedicated to leisure and purpose—barely existed.

Life was hard. Medicine was primitive. Public health systems were non-existent. Over the last 250 years, a revolution occurred—not in governance, but in biology. Through multiple generations, the curve of human history was permanently altered by the convergence of sanitation, vaccines, antibiotics, cardiovascular care, and breakthrough surgery.

The Longevity Reality: Then vs. Now

We have graduated from a society focused on survival to one increasingly mastering longevity.

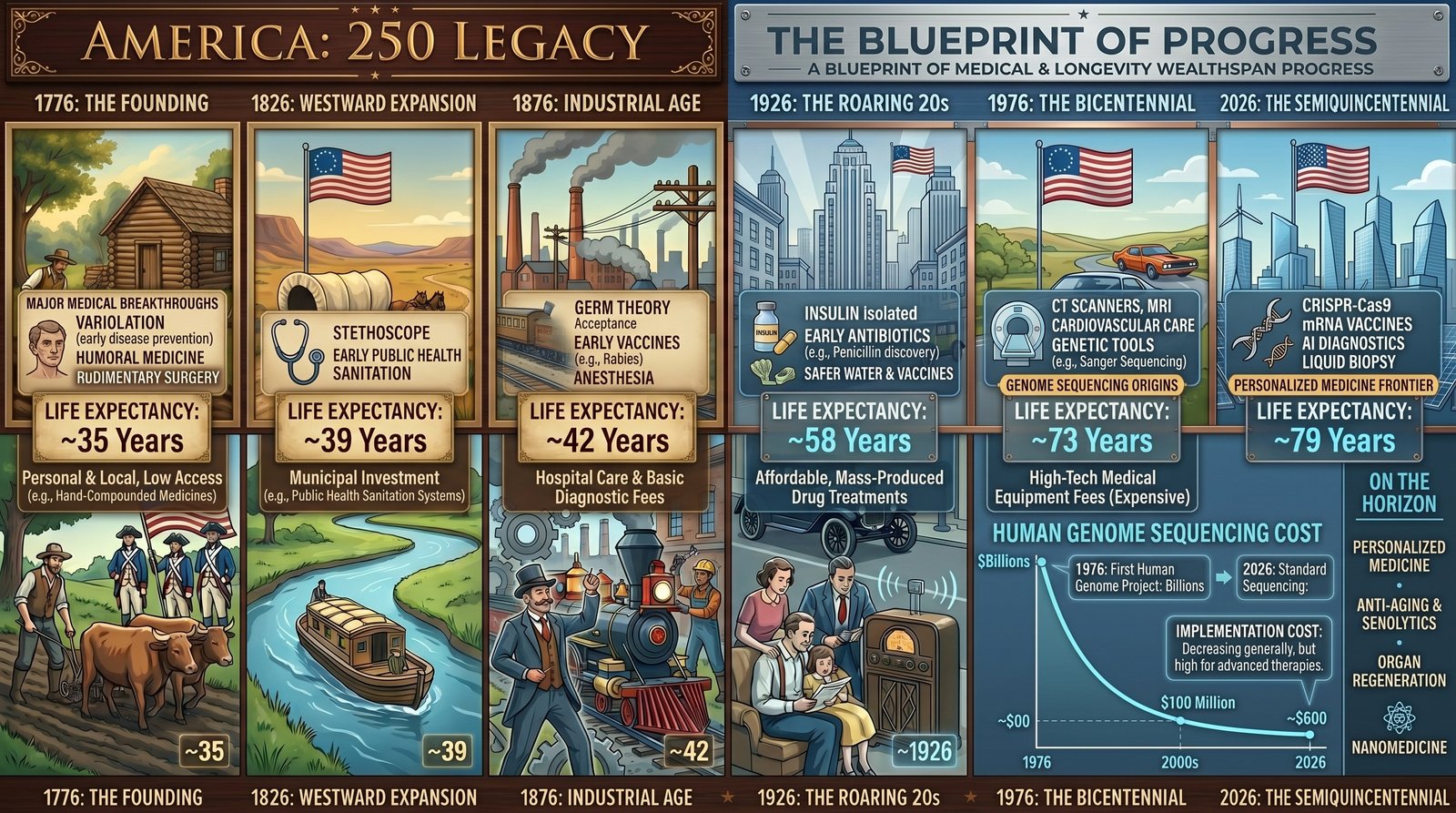

The trend is unmistakable. Historical data suggests that in the founding era of 1776, life expectancy at birth was roughly 35 to 40 years. Life was profoundly fragile. Fast-forward to 1926 (America at 150), and progress was underway, pushing life expectancy closer to 60. By 1976 (the Bicentennial), modern medicine and public health initiatives had reshaped expectations again, pushing the average lifespan to roughly 72.

Today, as we mark America’s 250th, a newborn’s expectancy is around 79 years. Crucially, a standard retiree at age 65 today must plan for approximately two decades—not years—beyond their working life. This is no longer the world of yesterday’s retirement assumptions.

Why Planning Must Evolve: The Scientific Accelerator

We are now entering an entirely new scientific phase that demands we abandon yesterday’s planning. Advanced genetics, precision medicine, biotechnology, artificial intelligence, and new screening capabilities are changing the human story again.

This is not a claim that human aging has been solved, but rather that it is moving from theory toward measurement. AI is accelerating biological modeling at unprecedented speed. Genetic tools are providing doctors and researchers with advanced risk identification. Breakthrough research, including work related to cellular reprogramming and “Yamanaka factors,” is exploring how specific aspects of aging might be slowed, repaired, or partially reversed.

If health technology is successful in extending healthy years, more people will need to prepare for a longer, more active life.

And that brings us to the most critical, yet overlooked, question of this era:

Will Your Money Last as Long as the Developments Suggest You Will?

This is the core realization that we believe most traditional financial advice has missed. We are at a turning point where a longer, more active life becomes a financial burden if your wealth, taxes, income strategy, healthcare coverage, estate plan, and family communication roadmap cannot keep pace.

Retirement planning can no longer be a rigid, linear spreadsheet calculation that ends on your 85th birthday. The tools, assumptions, and strategies used over the last 30 years were designed for an era of shorter life. They are outdated in a world where “Longevity Wealth Span” is the new mandate.

Your financial plan must evolve, or your retirement quality will suffer.

Integrating Healthspan and Wealthspan: A Smarter Roadmap

The point is not to create complexity for its own sake. The point is to stop managing health, money, taxes, care, and legacy in separate, outdated silos.

Healthspan is the period of life where you are functioning well—physically, mentally, socially, emotionally, and cognitively. Wealthspan is the period where your financial resources can support your lifestyle, independence, and choices without stress.

The goal is to live longer with options.

When we look at building a smarter, stronger plan together, we use a framework we call the Longevity Wealth Span Dashboard. It is designed specifically to address the seven connected questions a longer-life plan should answer:

Retirement Income: Where is the money coming from now, later, and for a surviving spouse for potentially 30+ years?

Social Security: How can claiming timing be optimized for maximum household lifetime benefit?

Taxes: Are Roth conversions, RMDs, capital gains, charitable strategies, and Medicare premium thresholds fully coordinated?

Investments: Is the portfolio built for long-term income, dynamic growth, liquidity, and inflation resilience?

Healthcare and Long-Term Care: What are the dynamic assumptions for Medicare, prescriptions, out-of-pocket costs, and potential care scenarios?

Insurance and Asset Protection: What risks could disrupt the entire strategy at an advanced age?

Estate and Legacy: Are documents, beneficiary designations, titling, charitable goals, and family communication aligned for transitions later in life?

A Legacy Worth Protecting

A wealthy retirement without health can feel frustrating. A healthy retirement without dynamic planning can feel financially stressful. The point of this national milestone, America at 250, is not to fix a precise expiration date. It is to recognize that the direction of travel for our society is toward longevity. If the next 50 years moves us toward healthier, more personalized aging, your financial plan has to evolve with it. The most common risk in financial planning today is not a market downturn; it is the possibility that your health succeeds but your financial roadmap cannot keep up.

We invite you to schedule a confidential consultation with our team to review your retirement roadmap and build a strategy that is built for longevity.

Disclosure: This content is for informational and educational purposes only and is not individualized medical, legal, tax, insurance, accounting, or individualized investment advice. Consult your physician and qualified professionals before making changes to your health, financial, tax, legal, insurance, or estate plan. This article discusses broad trends in longevity science and retirement planning. It does not suggest that any specific technology, therapy, supplement, screening, or medical intervention will extend life, cure disease, or be appropriate for any individual. Investing involves risk, including the possible loss of principal

Let’s build a stronger, smarter plan together.

Schedule your free consultation today

At AWM, Our Fiduciary Duty Principles™ Define Our Commitment

This commentary is for informational and educational purposes only and is not investment, tax, legal, or accounting advice. Any investment involves risk, including the possible loss of principal. Private and alternative investments may be illiquid, may involve higher fees, may use leverage, may have limited transparency, and may not be suitable for all investors. Liquidity features (including redemption/repurchase programs) are not guaranteed and may be limited, suspended, or modified. Distributions are not guaranteed and may be sourced from factors other than operating cash flow. Tax treatment is complex and investor-specific; consult your tax advisor. Any offering is made only through applicable offering documents and only to eligible investors where lawful.

How We Can Help You

At AWM, we provide personalized, comprehensive guidance for individuals and families. Our services offer peace of mind and confidence through every stage of your financial journey:

- Investment Management: Our globally diversified, tax-efficient portfolios are designed for resilience across market conditions.

- Proactive Tax Planning: We focus on tax-efficient strategies for both accumulation and distribution phases, helping you manage liabilities.

- Integrated Goals-Based Planning: Align all life goals into a unified financial plan to navigate transitions strategically.

Contact AWM today to schedule a confidential consultation and connect with an advisor who can help you achieve your financial goals. For assistance, reach out to us at Service@awmfl.com.

Thank you for your continued trust and engagement.

Tony Gomes, Author, MBA

CEO and Founder

Advanced Wealth Management