When the Headlines Get Loud, I Go Back to the Plan

Dear Clients and Friends,

Weekends like this are a reminder that markets do not exist in a vacuum.

Recent developments in the Middle East — including U.S. and Israeli military strikes on Iran — have understandably raised geopolitical concerns and, for many investors, the bigger question underneath the headline: What does this mean for my money, my retirement plan, and the road ahead?Before I say anything about markets, let me say something human first: I hope this situation ultimately leads to greater stability in the region and to better lives for the Iranian people. These events involve real people, real loss, real uncertainty, and far more than a ticker symbol on a screen.

That said, my job is not to provide military commentary or political editorializing. There are plenty of places to go for that. My job is to help families think clearly when headlines get emotional, markets get noisy, and the temptation to “do something” gets stronger than the actual need to do anything at all. So that is what this note is about.

- Not politics.

- Not cable-news adrenaline.

- Not hot takes dressed up as strategy.

Just a practical look at what I’m watching, what history suggests, what I’m doing in portfolios, and how I think long-term investors should respond.And my core message is simple:

Scary headlines are real. Panic is optional. Discipline still wins.

My first read on the market response: notable, but not panicked

When geopolitical risk spikes, I try to ignore the volume of the commentary and focus instead on the market’s actual behavior.That usually tells us more.The initial market reaction was exactly what you would expect: some overnight weakness, some nervousness at the open, and a sharp move higher in oil. None of that is surprising. But what stood out to me was what didn’t happen.

We did not see the kind of all-out flight to safety that usually shows up when investors believe a true systemic crisis is unfolding. In a classic fear event, I would expect Treasury prices to surge and yields to drop hard as people rush for cover. Instead, bond yields were firmer. Stocks, after the initial wobble, were much steadier than many would have guessed if they had only read the headlines.That does not mean there is no risk.It means the market, so far, appears to be treating this as a serious geopolitical event without yet pricing it as a full-scale global economic shock.That distinction matters.Because one of the easiest ways to damage a long-term plan is to treat every frightening headline as if it carries identical economic consequences.It doesn’t.

The real transmission mechanism here is oil

When investors hear “Middle East conflict,” the first market question is almost always oil. That’s appropriate. If this story affects the real economy, it is most likely to do so through energy prices, inflation expectations, transportation costs, consumer sentiment, and downstream pressure on goods and services.And yes, oil moved sharply.That is a rational response,But I want to make an important distinction here: oil volatility is not automatically the same thing as a lasting supply shock.

At this point, I see a few reasons not to jump straight to worst-case thinking:

- The global oil market appears better supplied than it was a year ago.

- Major producers had already signaled plans to increase output.

- There were no meaningful reports, in the analysis I reviewed, of major damage to Iranian oil infrastructure itself.

- And the U.S. gets very little direct oil supply from Iran in the first place.

In plain English: a sharp move in oil prices makes sense, but that alone does not prove we are entering an energy crisis.Now, could that change? Absolutely.If shipping routes were significantly disrupted for a multi-week period, if broader regional production were impaired, or if infrastructure damage spread beyond what we know today, then the economic conversation changes fast. That is why I am watching energy markets so closely.But as of now, I think the more reasonable base case is volatility, not automatic catastrophe.And that is an important distinction for investors trying to decide whether to stay disciplined or to start flailing.

My point is simpler and more useful:

Markets are forward-looking. Headlines are backward-looking.

The market starts digesting, repricing, and adapting long before the average person feels emotionally comfortable again.That is one reason why investors who wait for the all-clear often miss the recovery.

What history says about market shocks

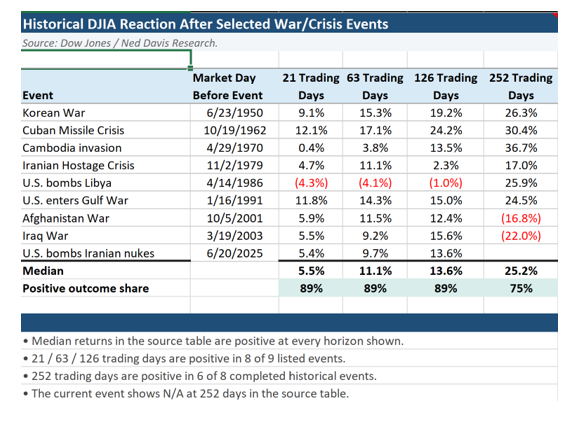

The first chart in this post is helpful because it narrows the focus.Instead of showing a giant multi-decade market history, it looks at the median stock-market response following a set of major geopolitical and war-related shock events.

And while no historical comparison is perfect, the pattern is instructive. Across the crisis events in that analysis, the median market return after the initial reaction was:

- +5.5% after 21 market days

- +11.1% after 63 market days

- +13.6% after 126 market days

- +25.2% after 252 market days

That is not a forecast. It is not a guarantee. And it is certainly not an invitation to ignore risk.What it is is a very useful reminder that selling into fear has historically been a poor strategy.Investors often assume the biggest danger comes from staying invested during scary periods. In reality, one of the biggest dangers is abandoning a sound plan right before the market stabilizes and recovers.

The lesson I take from that chart is not “nothing matters.”

The lesson is: do not confuse discomfort with evidence that your plan is broken.

The bigger chart tells the bigger story

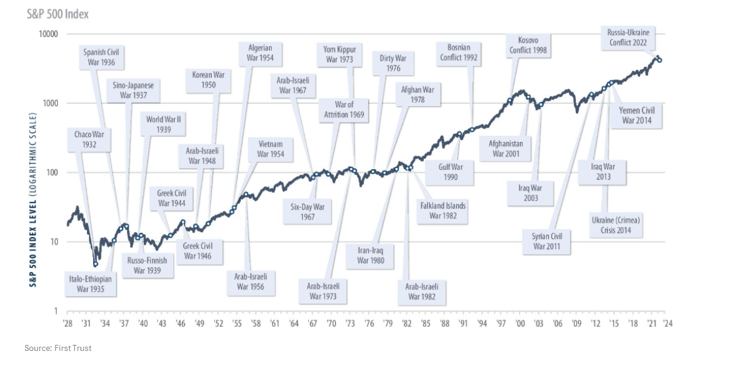

The second chart may be even more powerful because it zooms out.It shows the S&P 500 over many decades, with a long list of wars, regional conflicts, invasions, civil wars, and geopolitical flashpoints marked along the way. The reason I like this chart is that it provides the context investors often lose in the middle of a stressful week.

The market has lived through:

- Wars,

- Terror attacks,

- Oil shocks,

- Recessions,

- Inflation scares,

- Sovereign crises,

- Banking panics,

- Political instability,

- And more “this changes everything” moments than any of us can count.

And yet the long-term trajectory, despite all of it, has still been higher.Again, I want to be clear: I am not saying every conflict is investable background noise. I am saying the stock market’s long-term drivers have historically been things like:

- Productivity,

- Innovation,

- Earnings,

- Human adaptation,

- And the tendency of businesses and economies to keep moving forward after shocks.

The market may stumble. It may correct. It may overshoot in both directions. But over long periods of time, the arc has been resilience.

When I look at that chart, I do not see permission to be complacent.I see a reminder to keep perspective.

What concerns me more than the headline itself

Now let me add some nuance, because this is where lazy commentary usually falls apart.Even if I do not believe this specific event automatically leads to a lasting market crisis, I also do not think the backdrop was exactly stress-free before this happened.That is what investors need to remember.

This conflict landed on top of a market that was already working through a number of important pressure points:

- Elevated valuations in parts of the market,

- Sticky inflation in certain categories,

- Tariff-related pricing pressure,

- Ongoing questions about AI investment versus actual monetization,

- Some credit complacency,

- And a lot of investor confidence that had been getting fairly cozy.

So while I am not interested in panic, I am also not interested in pretending this event occurred in a vacuum.Sometimes the geopolitical event is not the entire problem. Sometimes it is the extra strain added to an already stretched system.That is why I think simplistic comparisons — “stocks went up during X war, so this is bullish” — are not helpful. Markets do not operate on history memes. Context matters. Valuation matters. rates matter. earnings matter. oil matters. liquidity matters.This is why portfolio construction matters too.

This is exactly why I believe in diversified, all-weather planning

One of the most important things I want clients to understand is that a well-built portfolio is not designed only for calm weather.It is supposed to be built for uncomfortable stretches too.Diversification is easy to ignore when one slice of the market is flying and everything feels obvious. But diversification earns its keep when markets remind us that uncertainty can come from anywhere and on any schedule.

That is why I continue to believe in:

- Diversification across asset classes,

- Diversification across geographies,

- Quality exposure over speculation,

- Appropriate liquidity,

- And making sure the portfolio serves the plan — not the other way around.

Different assets can respond differently to geopolitical stress. Some areas may benefit. Some may lag. Some may simply provide ballast. The goal is not to predict every short-term winner. The goal is to build something resilient enough that you do not feel forced into emotional decisions every time the news cycle goes into full drama mode. And let’s be honest: the news cycle is always in full drama mode. If cable news had a portfolio, it would be 100% allocated to urgency.

What I’m doing right now in the portfolios I oversee

In moments like this, I do not become more theatrical. I become more methodical.Here is what that looks like for me right now.

1) I’m reviewing risk through the lens of the plan, not the headline

I care less about whether a scary event happened and more about whether it meaningfully changes the long-term assumptions behind a client’s plan.

- Does it change cash-flow needs?

- Does it change retirement-income timing?

- Does it change liquidity needs?

- Does it change expected inflation pressure?

- Does it change the role each account is supposed to play?

That is the work.

2) I’m paying close attention to oil, inflation, and second-order effects

The biggest short-term market impact from this situation is likely to come through energy. If energy stays elevated, it can feed into transportation, manufacturing, consumer sentiment, and inflation expectations.That does not mean we overreact. It means we pay attention and update our thinking honestly.

3) I’m not chasing the “obvious” trade

Yes, defense stocks can pop in moments like this. Energy can spike. LNG exposure can catch a bid. Those moves are understandable.But one of the oldest ways to lose money is to arrive late to the trade everyone suddenly agrees is obvious.I am not interested in turning client portfolios into headline-chasing machines. That is not strategy. That is just expensive adrenaline.

4) I’m revisiting liquidity and income planning

This is where real financial planning beats market commentary.People do not retire on a market opinion.They retire on a cash-flow strategy.So in periods like this, I always come back to the income plan:

- What is needed in the next 12 months?

- What is already covered?

- What should remain liquid?

- What can remain invested?

- What does the client actually need to feel secure?

Those are the questions that matter far more than whether the market is green or red on a single Monday.

5) I’m continuing to think beyond public markets where appropriate

This kind of environment is also a reminder that public markets are not the only lever in a portfolio.For the right investor, institutional private investments can play a role alongside traditional public stocks and bonds. That may include private real estate, private credit, or private equity — always sized appropriately, matched to liquidity needs, and evaluated within the context of taxes, income needs, and long-term goals.

That is not about using complexity for complexity’s sake. It is about using the right tools for the right job.And it is one reason I built our Private Market Alpha Guide in the first place — to help families understand how affluent investors often think about opportunities beyond what shows up on a standard brokerage menu.

What I am not recommending

Sometimes it helps to say this plainly.I am not recommending:

- Panic selling,

- All-in market timing,

- Dumping diversification because one sector popped,

- Pretending oil doesn’t matter,

- Or making long-term changes because the weekend headlines were emotionally intense.

I am also not recommending that investors numb themselves with fake certainty, There is still uncertainty here. The situation is fluid. Markets can reprice quickly. Oil can move further. Volatility can increase.But uncertainty is not a reason to abandon process. It is a reason to lean on it.

If this week made you realize you want a better framework, start here

One of the reasons I spend so much time building educational tools is because I know uncertainty is easier to handle when you already have a framework.The families who tend to navigate stressful periods best are not the ones who magically predict every crisis. They are the ones who already know:

- Where their income is coming from,

- How much liquidity they have,

- What their portfolio is designed to do,

- What role taxes play,

- And which decisions deserve action versus patience.

If this recent stretch of volatility has you wanting a better planning framework, start with the tools I built specifically for that purpose.

- Retirement Playbook — a practical starting point for retirement income, structure, and next-step planning.

- Private Market Alpha Guide — for those curious how affluent families use institutional private investments as part of a broader plan.

- Social Security Quick-Start — for people trying to avoid turning a lifetime benefit into a rushed decision.

- Estate Planning Simplified — because too many families think “we did our estate plan” when what they really mean is “we signed papers once.”

- Mega Backdoor Roth — for high earners trying to maximize tax-efficient savings without turning it into a science fair project.

I built these resources for one reason:

I want you to make calm decisions before stress shows up — not reactive ones after it does.

My bottom line

Here is where I land today.

This is a serious geopolitical development. It deserves attention. It deserves humility. It deserves prayer for the safety of innocent people and for greater stability in the region.From an investment standpoint, though, I do not believe this is a moment for impulsive portfolio changes based on fear alone. The market response so far has been more measured than the headlines suggest. Oil is the key channel to watch, but we are not automatically in a full supply-shock scenario. History shows that markets have repeatedly processed geopolitical stress and continued higher over time. And, as always, the investors most likely to be rewarded are usually the ones who stay disciplined when everyone else is tempted to get dramatic.

That is why I keep coming back to the same message:

Look through the noise. Go back to the plan. Stay diversified. Stay disciplined. Stay focused on the long term.

If you are already a client, know that I am watching this closely and doing what I always do: separating signal from noise and making sure your portfolio remains aligned with your goals. If we are not yet working together and you would like a second opinion, start with the educational resources, then book a complimentary consultation and I will be happy to review your situation with you.Because in uncertain times, clarity is valuable.And calm, informed decision-making is even more valuable.

— Tony Gomes

Let’s build a stronger, smarter plan together.

Schedule your free consultation today

At AWM, Our Fiduciary Duty Principles™ Define Our Commitment

This commentary is for informational and educational purposes only and is not investment, tax, legal, or accounting advice. Any investment involves risk, including the possible loss of principal. Private and alternative investments may be illiquid, may involve higher fees, may use leverage, may have limited transparency, and may not be suitable for all investors. Liquidity features (including redemption/repurchase programs) are not guaranteed and may be limited, suspended, or modified. Distributions are not guaranteed and may be sourced from factors other than operating cash flow. Tax treatment is complex and investor-specific; consult your tax advisor. Any offering is made only through applicable offering documents and only to eligible investors where lawful.

How We Can Help You

At AWM, we provide personalized, comprehensive guidance for individuals and families. Our services offer peace of mind and confidence through every stage of your financial journey:

- Investment Management: Our globally diversified, tax-efficient portfolios are designed for resilience across market conditions.

- Proactive Tax Planning: We focus on tax-efficient strategies for both accumulation and distribution phases, helping you manage liabilities.

- Integrated Goals-Based Planning: Align all life goals into a unified financial plan to navigate transitions strategically.

Contact AWM today to schedule a confidential consultation and connect with an advisor who can help you achieve your financial goals. For assistance, reach out to us at Service@awmfl.com.

Thank you for your continued trust and engagement.